Start Understanding Why Life Insurance Matters More Than You Think

For many Malaysians, life insurance is seen as a future concern, reserved for later stages or significant milestones. In reality, it is a crucial safeguard for life's unexpected twists. It’s a way to protect the life you’ve directed so far.

What Happens When Main Income Stops Suddenly?

Immediate Financial Strain: Daily expenses like groceries, utilities and rent or mortgage payments can become difficult.

Depletion of Savings: Families may need to use savings to meet basic expenses, which can quickly diminish emergency funds and long-term savings between 6 to 12 months.

Increased Debt: Families may rely on credit cards or loans to make ends meet, leading to increased debt and financial stress.

Lifestyle Adjustments: Families might make significant lifestyle changes, such as cutting back on non-essential spending, selling assets or downsizing their living arrangements overall.

Emotional and Psychological Impact: Financial stress can lead to anxiety and tension within the household, affecting relationships and overall well-being.

Long-term Financial Goals: Plans for the future like buying a home, funding children’s education or saving for retirement may be delayed or compromised.

Do you know that as at 2024, only 2 out of 5 Malaysians have life protection? Are you one of them?

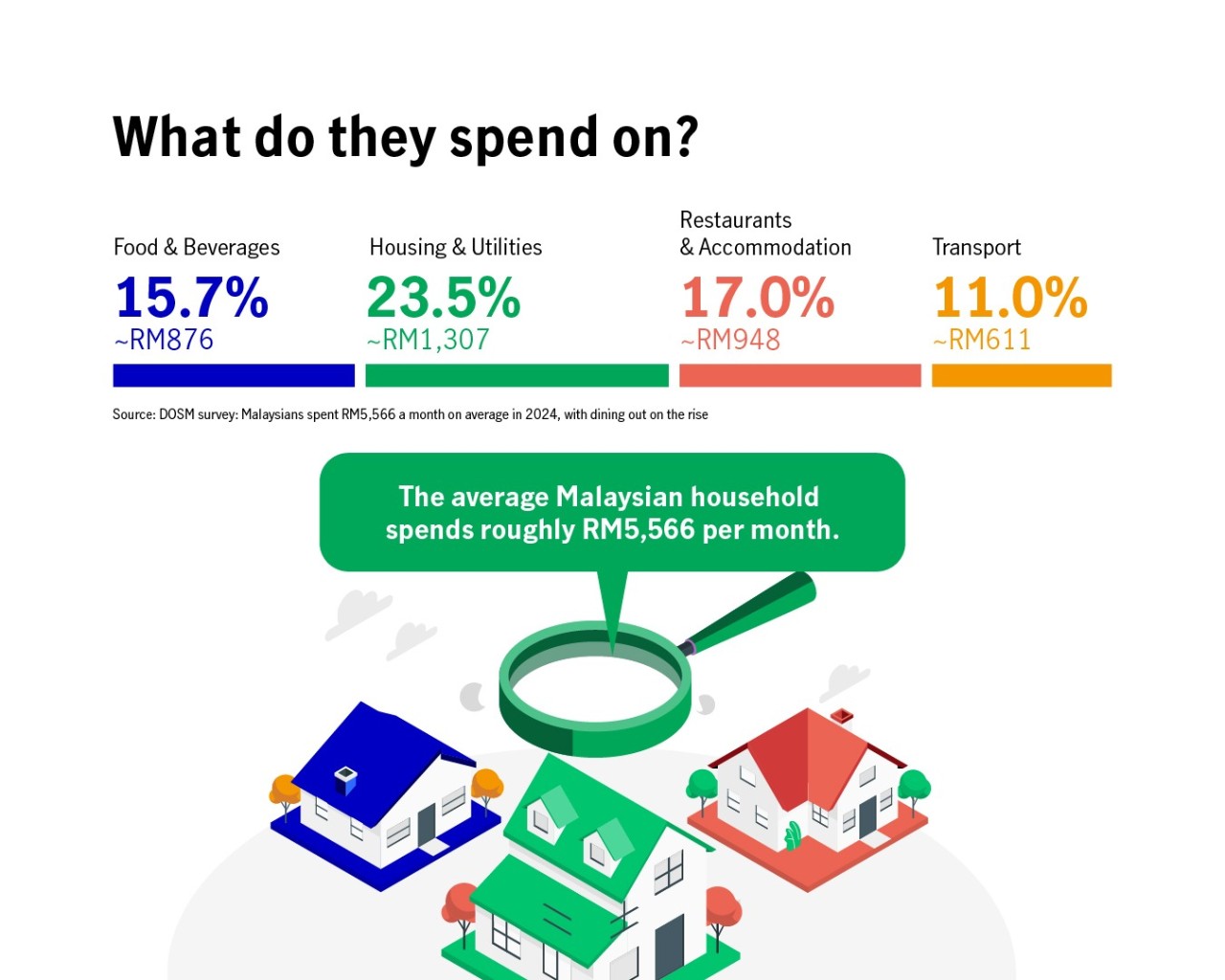

With life expectancy reaching 74.8 years in 2023 and Malaysia projected to become an aged nation by 2044, the protection gap is widening. At the same time, the latest Household Income and Expenditure Survey (HIES) 2024 reports average monthly household spending of RM5,566, highlighting the potential financial strain families may face without adequate coverage and the urgent need to review and strengthen life protection.

Considering buying life insurance later also means higher premiums, making coverage less affordable. Manulife offers solutions that help you start building your protection pot today, ensuring your family is safeguarded without compromising your budget.

What Are The Key Benefits of Life Insurance?

With the financial pressures faced by many Malaysian households, having the right protection in place becomes even more essential. Life insurance may help to cushion families against sudden income disruptions and may ensure long-term responsibilities remain manageable by:

- Providing financial stability for families who rely on a main income earner.

- Covering ongoing daily expenses when income is suddenly lost.

- Acting as a financial buffer so families can adjust to their new financial situation.

- Ensuring long‑term obligations can still be managed, such as housing loans or children’s education.

- Supporting shared financial commitments between spouses or family members.

- Offering flexibility across different life stages, not just short‑term goals.

Does Starting Early Really Make A Difference?

Yes! Getting life insurance earlier often means your entry premium will be lower because insurers generally charge less when you are younger and healthier. Buying early also makes it easier to qualify at standard rates without medical loadings and lets you lock in insurability before any health changes occur. These factors can make premiums cheaper at the start compared to buying a policy at an older age

Certain Investment-Linked Policies (ILPs) may offer the potential for returns to grow over time. By starting early, you benefit from affordability, flexibility and the opportunity for your policy to grow in line with your life and income.

How Do I Know Which Life Insurance Should I Go For?

Choosing the right policy depends on your goals and priorities.

Life insurance is not just about expecting bad things to happen. It is about making sure the important things in your life like your family and your plans are safe. If something unexpected happens, life insurance helps make sure that your financial duties do not suddenly become a problem for you and your loved ones.

Frequently Asked Questions (FAQs) about life insurance

At what point do you need life insurance?

People typically start considering life insurance when their financial responsibilities grow and others may be affected by changes in their income, such as: taking on long‑term commitments, supporting family members or planning ahead for future stability. Obtaining coverage earlier in life may make it easier to secure affordable protection, but it ultimately depends on each person's needs and circumstances.

Can I withdraw money from my life insurance?

Some life insurance plans allow withdrawals, but it depends on the type of policy you have. Any withdrawal may reduce your coverage, so it is worth reviewing how it could affect your long‑term protection before making a decision.

What type of death is not covered by life insurance?

Coverage can vary by policy, but most life insurance plans have certain exclusions. These may include situations like suicide within the policy’s early period or deaths linked to high‑risk activities not included in the coverage. Some policies may also exclude deaths related to illegal activities. It is always worth checking the specific terms of your plan to understand what is or is not covered.

Who really needs life insurance?

Life insurance may be worth considering for anyone with financial responsibilities that could affect others. This may include people supporting family members, managing shared commitments or planning ahead for long‑term stability. Even individuals without dependents should explore coverage as part of broader financial planning. Ultimately, the need varies based on personal circumstances, goals and how much financial protection someone wants to have in place.

Here’s how you can better direct your life ahead with Manulife

* PROTECTION BY PIDM ON BENEFITS PAYABLE FROM THE UNIT PORTION OF THIS PRODUCT IS SUBJECT TO LIMITATIONS. Please refer to PIDM’s TIPS Brochure or contact Manulife Insurance Berhad or PIDM (visit www.pidm.gov.my).

** The benefit(s) payable under eligible product is protected by PIDM up to limits. Please refer to PIDM’s TIPS Brochure or contact Manulife Insurance Berhad or PIDM (visit www.pidm.gov.my).

If you liked this article, we recommend you to continue reading

Thank you {FirstName} for contacting Manulife!

We will be in touch with you soon

Your Reference number: {ReferenceID}

Oops!

Error 404

Please excuse us

Sorry. We are processing a few things behind the scene. Please try again in a few moments.

But wait, here are some links we think might interest you:

© 2020–2026 Manulife Holdings Berhad (Registration No. 197501003360 (24851-H))

General Line : (603) 2719 9228 | Customer Careline : 1 300 13 2323

Manulife Insurance Berhad ([Company No. 200801013654] (814942-M) is a member of PIDM.